A disruptive technology or disruptive innovation is an innovation that helps create a new market and value network, and eventually goes on to disrupt an existing market and value network. The term is used in business and technology literature to describe innovations that improve a product or service in ways that the market does not expect. Although the term disruptive technology is widely used, disruptive innovation seems a more appropriate term in many contexts since few technologies are intrinsically disruptive; rather, it is the business model that the technology enables that creates the disruptive impact.

17.1 Introduction

How can I beat my most powerful competitor? How can I know in advance of the battle whether I’m going to be able to beat the competition? Why has disruption proven to be such a consistently effective strategy for causing strong incumbent competitors to flee from their entrant attackers, rather than fight them? How can I shape a business idea into a disruptive strategy?

What if you could predict the winners in a race for innovative growth? What if you could choose your competitive battles knowing you would win nearly every time? What if you knew in advance which growth strategies would succeed, and which would fail?

Managers have long sought ways to predict the outcome of competitive fights. Some look at the attributes of the companies involved: Larger companies with more resources to throw at a problem will beat the smaller competitors. It’s interesting how often the CEOs of large, resource-rich companies base their strategies upon this theory, despite repeated evidence that the level of resources committed often bears little relationship to the outcome.

Others consider the attributes of the change: When innovations are incremental, the established, leading firms in an industry are likely to reinforce their dominance; however, compared with entrants, they will be conservative and ineffective in exploiting breakthrough innovation (footnote 1).

Our ongoing study of innovation suggests another way to understand when incumbents will win, and when the entrants are likely to beat them. The Innovator’s Dilemma (Christensen 1997) identified two distinct categories-sustaining and disruptive-based on the circumstances of innovation. In sustaining situations-when the race entails making better products that can be sold for more money to attractive customers-we found that incumbents almost always prevail. In disruptive circumstances-when the challenge is to commercialize a simpler, more convenient product that sells for less money and appeals to a new or unattractive customer set-the entrants are likely to beat the incumbents. This is the phenomenonthat so frequently defeats successful companies. It implies, of course, that the best way for upstarts to attack established competitors is to disrupt them.

Few technologies or business ideas are intrinsically sustaining or disruptive in character. Rather, their disruptive impact must be molded into strategy as managers shape the idea into a plan and then implement it. Successful new-growth builders know-either intuitively or explicitly-that disruptive strategies greatly increase the odds of competitive success.

This chapter’s purpose is to review the disruptive innovation model from the perspective of both the disruptee and the disruptor in order to help growth builders shape their strategies so that they pick disruptive fights they can win. Because disruption happens whether we want it or not, this chapter should also help established companies capture disruptive growth, instead of getting killed by it.

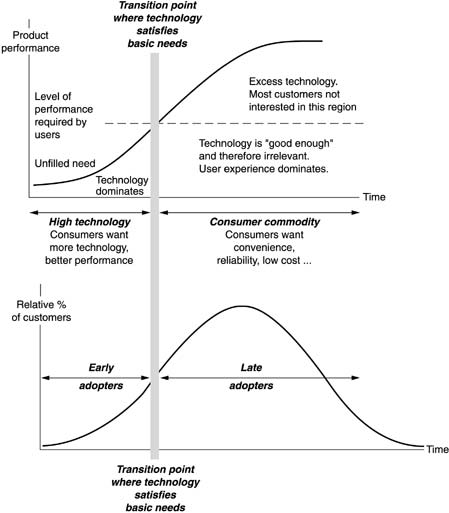

17.2 The Disruptive Innovation Model

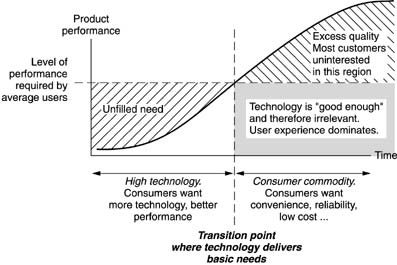

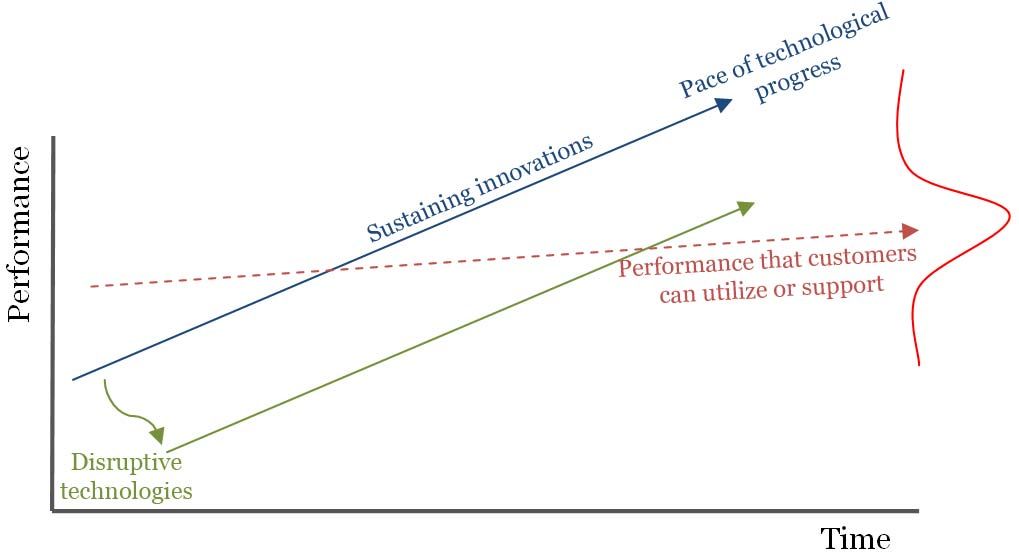

The Innovator’s Dilemma (Christensen 1997) identified three critical elements of disruption, as depicted in Figure 1. First, in every market there is a rate of improvement that customers can utilize or absorb, represented by the dotted line sloping gently upward across the chart. For example, the automobile companies keep giving us new and improved engines, but we can’t utilize all the performance that they make available under the hood. Factors such as traffic jams, speed limits, and safety concerns constrain how much performance we can use.

Author/Copyright holder: Clayton Christensen. Copyright terms and licence: All Rights Reserved. Reproduced with permission. See section "Exceptions" in the copyright terms below.

Figure 17.1: The Disruptive Innovation Model

To simplify the chart, we depict customers’ ability to utilize improvement as a single line. In reality, there is a distribution of customers around this median: There are many such lines, or tiers, in a market-a range indicated by the distribution curve at the right. Customers in the highest or most demanding tiers may never be satisfied with the best that is available, and those in the lowest or least demanding tiers can be over-satisfied with very little. But on average, this dotted line represents technology that is “good enough” to serve existing mainstream customers’ needs.

Second, in every market there is a distinctly different trajectory of improvement that innovating companies provide as they introduce new and improved products. The more steeply sloping solid lines in Figure 1 suggest that this pace of technological progress almost always outstrips the ability of customers in any given tier of the market to use it. Thus, a company whose products are squarely positioned on mainstream customers’ current needs will probably overshoot what those same customers are able to utilize in the future. This happens because companies keep striving to make better products that they can sell for higher profit margins to not-yet-satisfied customers in more demanding tiers of the market.

To visualize this, think back to 1983 when people first started using personal computers for word processing. Typists often had to stop their fingers to let the Intel 286 chip inside catch up. As depicted at the left side of Figure 1, the technology was not good enough. But today’s processors offer much more speed than mainstream customers can use-although there are still a few unsatisfied customers in the most demanding tiers of the market who need even-faster chips.

The third critical element of the model is the distinction between sustaining and disruptive innovation. A sustaining innovation targets demanding, high-end customers with better performance than what was previously available. Some sustaining innovations are the incremental year-by-year improvements that all good companies grind out. Other sustaining innovations are breakthrough, leapfrog-beyond-the-competition products. It doesn’t matter how technologically difficult the innovation is, however: The established competitors almost always win the battles of sustaining technology. Because this strategy entails making a better product that they can sell for higher profit margins to their best customers, the established competitors have powerful motivations to fight sustaining battles. And they have the resources to win.

Disruptive innovations, in contrast, don’t attempt to bring better products to established customers in existing markets. Rather, they disrupt and redefine that trajectory by introducing products and services that are not as good as currently available products. But disruptive technologies offer other benefits-typically, they are simpler, more convenient, and less expensive products that appeal to new or less-demanding customers (footnote 3).

Once the disruptive product gains a foothold in new or low-end markets, the improvement cycle begins. And because the pace of technological progress outstrips customers’ abilities to use it, the previously not-good-enough technology eventually improves enough to intersect with the needs of more demanding customers. When that happens, the disruptors are on a path that will ultimately crush the incumbents. This distinction is important for innovators seeking to create new-growth businesses. Whereas the current leaders of the industry almost always triumph in battles of sustaining innovation, the odds at disruptive innovation heavily favor entrant companies (footnote 4).

Disruption has a paralyzing effect on industry leaders. With resource allocation processes designed and perfected to support sustaining innovations, they are constitutionally unable to respond. They are always motivated to go up-market, and almost never motivated to defend the new or low-end markets that the disruptors find attractive. We call this phenomenon asymmetric motivation. It is the core of the innovator’s dilemma, and the beginning of the innovator’s solution.

17.2.1 Disruption at Work: How Minimills Upended Integrated Steel Companies

The disruption of integrated steel mills by minimills, which is reviewed briefly in The Innovator’s Dilemma (Christensen 1997), offers a classic example of why established leaders are so much easier to beat if the idea for a new product or business is shaped into a disruption.

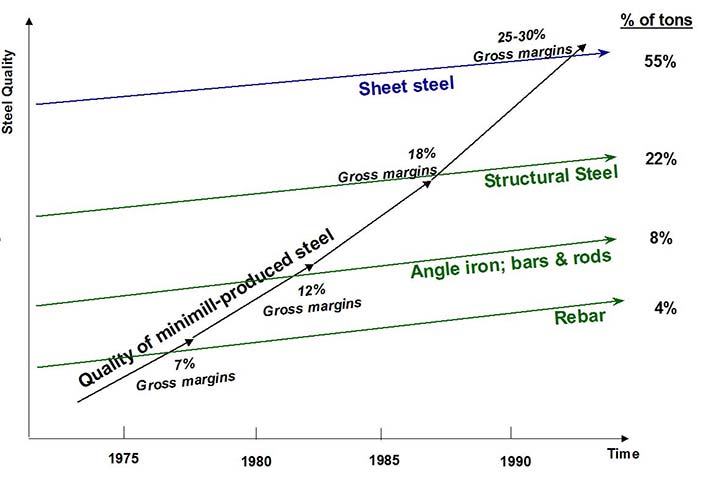

Historically, most of the world’s steel has come from massive integrated mills that do everything from reacting iron ore, coke, and limestone in blast furnaces to rolling finished products at the other end. It costs about $8 billion to build a huge new integrated mill today. Minimills, in contrast, melt scrap steel in electric arc furnaces-cylinders that are approximately twenty meters in diameter and ten meters tall. Because they can produce molten steel cost-effectively in such a small chamber, minimills don’t need the massive-scale rolling and finishing operations that are required to handle the output of efficient blast furnaces-which is why they are called minimills. Most important, though, minimills’ straightforward technology can make steel of any given quality for 20 percent lower cost than an integrated mill.

Steel is a commodity. You would think that every integrated steel company in the world would have aggressively adopted the straightforward, lower-cost minimill technology. Yet as of 2000 not a single integrated steel company had successfully invested in a minimill, even as the minimills had grown to account for nearly half of North America’s steel production and a significant share of other markets as well (footnote 5).

We can explain why something that makes so much sense has been so difficult for the integrated mills. Minimills first became technologically viable in the mid-1960s. Because they melt scrap of uncertain and varying chemistry in their electric arc furnaces, the quality of the steel that minimills initially could produce was poor. In fact, the only market that would accept the output of minimills was the concrete reinforcing bar (rebar) market. The specifications for rebar are loose, so this was an ideal market for products of low and variable quality.

As the minimills attacked the rebar market, the integrated mills were happy to be rid of that dog-eat-dog commodity business. Because of the differences in their cost structures and the opportunities for investment that they each faced, the rebar market looked very different to the disruptee and the disruptor. For integrated producers, gross profit margins on rebar often hovered near 7 percent, and the entire product category accounted for only 4 percent of the industry’s tonnage. It was the least attractive of any tier of the market in which they might invest to grow. So as the minimills established a foothold in the rebar market, the integrated mills reconfigured their rebar lines to make more profitable products.

In contrast, with a 20 percent cost advantage, the minimills enjoyed attractive profits in competition against the integrated mills for rebar-until 1979, when the minimills finally succeeded in driving the last integrated mill out of the rebar market. Historical pricing statistics show that the price of rebar then collapsed by 20 percent. As long as the minimills could compete against higher-cost integrated mills, the game was profitable for them. But as soon as low-cost minimill was pitted against low-cost minimill in a commodity market, the reward for victory was that none of them could earn attractive profits in rebar (footnote 6). Worse, as they all sought profitability by becoming more efficient producers, they discovered that cost reductions meant survival, but not profitability, in a commodity such as rebar (footnote 7).

Soon, however, the minimills looked up-market, and what they saw there spelled relief. If they could just figure out how to make bigger and better steel-shapes like angle iron and thicker bars and rods-they could roll tons of money, because in that tier of the market, as suggested in Figure 2, the integrated mills were earning gross margins of about 12 percent-nearly double the margins that they had been able to earn in rebar. That market was also twiceas big as the rebar segment, accounting for about 8 percent of industry tonnage. As the minimills figured out how to make bigger and better steel and attacked that tier of the market, the integrated mills were almost relieved to be rid of the bar and rod business as well. It was a dog-eat-dog commodity compared with their higher-margin products, whereas for the minimills, it was an attractive opportunity compared with their lower-margin rebar. So as the minimills expanded their capacity to make angle iron and thicker bars and rods, the integrated mills shut their lines down or reconfigured them to make more profitable products. With a 20 percent cost advantage, the minimills enjoyed significant profits in competition against the integrated mills until 1984, when they finally succeeded in driving the last integrated mill out of the bar and rod market. Once again, the minimills reaped their reward: With low-cost minimill pitted against low-cost minimill, the price of bar and rod collapsed by 20 percent, and they could no longer earn attractive profits. What could they do?

Author/Copyright holder: Clayton Christensen. Copyright terms and licence: All Rights Reserved. Reproduced with permission. See section "Exceptions" in the copyright terms below.

Figure 17.2: The Disruptive Attack of the Steel Minimills

Continued up-market movement into structural beams appeared to be the next obvious answer. Gross margins in that sector were a whopping 18 percent, and the market was three times as large as the bar and rod business. Most industry technologists thought minimills would be unable to roll structural beams. Many of the properties required to meet the specifications for steel used in building and bridge construction were imparted to the steel in the rolling processes of big integrated mills, and you just couldn’t get those properties in minimills’ abbreviated facilities. What the technical experts didn’t count on, however, was how desperately motivated the minimills would be to solve that problem, because it was the only way they could make attractive money. Minimills achieved extraordinarily clever innovations as they stretched from angle iron to I-beams-things such as Chaparral Steel’s dog-bone mold in its continuous caster, which no one had imagined could be done. Although you could never have predicted what the technical solution would be, you could predict with perfect certainty that the minimills were powerfully motivated to figure it out. Necessity remains the mother of invention.

At the beginning of their invasion into structural beams, the biggest that the minimills could roll were little six-inch beams of the sort that under-gird mobile homes. They attacked the low end of the structural beam market, and again the integrated mills were almost relieved to be rid of it. It was a dog-eat-dog commodity compared with their other higher-margin products where focused investment might bring more attractive volume. To the minimills, in contrast, it was an attractive product compared with the margins they were earning on rebar and angle iron. So as the minimills expanded their capacity to roll structural beams, the integrated mills shut their structural beam mills down in order to focus on more profitable sheet steel products. With a 20 percent cost advantage, the minimills enjoyed significant profits as long as they could compete against the integrated mills. Then in the mid-1990s, when they finally succeeded in driving the last integrated mill out of the structural beam market, pricing again collapsed. Once again, the reward for victory was the end of profit.

The sequence repeated itself when the leading minimill, Nucor, attacked the sheet steel business. Its market capitalization now dwarfs that of the largest integrated steel company, US Steel. Bethlehem Steel is bankrupt at the time of this writing.

This is not a history of bungled steel company management. It is a story of rational managers facing the innovator’s dilemma: Should we invest to protect the least profitable end of our business, so that we can retain our least loyal, most price-sensitive customers? Or should we invest to strengthen our position in the most profitable tiers of our business, with customers who reward us with premium prices for better products?

The executives who confront this dilemma come in all varieties: timid, feisty, analytical, and action-driven. In an unstructured world their actions might be unpredictable. But as large industry incumbents, they encounter powerful and predictable forces that motivate them to flee rather than fight when attacked from below. That is why shaping a business idea into a disruption is an effective strategy for beating an established competitor. Disruption works because it is much easier to beat competitors when they are motivated to flee rather than fight.

The forces that propel well-managed companies up-market are always at work, in every company in every industry. Whether or not entrant firms have disrupted the established leaders yet, the forces are at work, leading predictably in one direction. It is not just a phenomenon of “technology companies” such as those involved in microelectronics, software, photonics, or biochemistry. Indeed, when we use the term technology in this chapter, it means the process that any company uses to convert inputs of labor, materials, capital, energy, and information into outputs of greater value. For the purpose of predictably creating growth, treating “high tech” as different from “low tech” is not the right way to categorize the world. Every company has technology, and each is subject to these fundamental forces.

17.2.2 The Role of Sustaining Innovation in Generating Growth

We must emphasize that we do not argue against the aggressive pursuit of sustaining innovation. Several other insightful books offer management techniques to help companies excel in sustaining innovations-and their contribution is important (footnote 8). Almost always a host of similar companies enters an industry in its early years, and getting ahead of that crowd-moving up the sustaining-innovation trajectory more decisively than the others-is critical to the successful exploitation of the disruptive opportunity. But this is the source of the dilemma: Sustaining innovations are so important and attractive, relative to disruptive ones, that the very best sustaining companies systematically ignore disruptive threats and opportunities until the game is over.

Sustaining innovation essentially entails making a better mousetrap. Starting a new company with a sustaining innovation isn’t necessarily a bad idea: Focused companies sometimes can develop new products more rapidly than larger firms because of the conflicts and distractions that broad scope often creates. The theory of disruption suggests, however, that once they have developed and established the viability of their superior product, entrepreneurs who have entered on a sustaining trajectory should turn around and sell out to one of the industry leaders behind them. If executed successfully, getting ahead of the leaders on the sustaining curve and then selling out quickly can be a straightforward way to make an attractive financial return. This is common practice in the health care industry, and was the well-chronicled mechanism by which Cisco Systems “outsourced” (and financed with equity capital, rather than expense money) much of its sustaining-product development in the 1990s.

A sustaining-technology strategy is not a viable way to build new-growth businesses, however. If you create and attempt to sell a better product into an established market to capture established competitors’ best customers, the competitors will be motivated to fight rather than to flee (footnote 9). This advice holds even when the entrant is a huge corporation with ostensibly deeper pockets than the incumbent.

For example, electronic cash registers were a radical but sustaining innovation relative to electromechanical cash registers, whose market was dominated by National Cash Register (NCR). NCR totally missed the advent of the new technology in the 1970s-so badly, in fact, that NCR’s product sales literally went to zero. Electronic registers were so superior that there was no reason to buy an electromechanical product except as an antique. Yet NCR survived on service revenues for over a year, and when it finally introduced its own electronic cash register, its extensive sales organization quickly captured the same share of the market as the company had enjoyed in the electromechanical realm (footnote 10). The attempts that IBM and Kodak made in the 1970s and 1980s to beat Xerox in the high-speed photocopier business are another example. These companies were far bigger, and yet they failed to outmuscle Xerox in a sustaining-technology competition. The firm that beat Xerox was Canon-and that victory started with a disruptive tabletop copier strategy.

Similarly, corporate giants RCA, General Electric, and AT&T failed to outmuscle IBM on the sustaining-technology trajectory in mainframe computers. Despite the massive resources they threw at IBM, they couldn’t make a dent in IBM’s position. In the end, it was the disruptive personal computer makers, not the major corporations who picked a direct, sustaining-innovation fight, that bested IBM in computers. Airbus entered the commercial airframe industry head-on against Boeing, but doing so required massive subsidies from European governments. In the future, the most profitable growth in the airframe industry will probably come from firms with disruptive strategies, such as Embraer and Bombardier’s Canadair, whose regional jets are aggressively stretching up-market from below (footnote 11).

17.2.3 Disruption Is a Relative Term

An idea that is disruptive to one business may be sustaining to another. Given the stark odds that favor the incumbents in the sustaining race but entrants in disruptive ones, we recommend a strict rule: If your idea for a product or business appears disruptive to some established companies but might represent a sustaining improvement for others, then you should go back to the drawing board. You need to define an opportunity that is disruptive relative to all the established players in the targeted market space, or you should not invest in the idea. If it is a sustaining innovation relative to the business model of a significant incumbent, you are picking a fight you are very unlikely to win.

Take the Internet, for example. Throughout the late 1990s, investors poured billions into Internet-based companies, convinced of their “disruptive” potential. An important reason why many of them failed was that the Internet was a sustaining innovation relative to the business models of a host of companies. Prior to the advent of the Internet, Dell Computer, for example, sold computers directly to customers by mail and over the telephone. This business was already a low-end disruptor, moving up its trajectory. Dell’s banks of telephone salespeople had to be highly trained in order to walk their customers through the various configurations of components that were and were not feasible. They then manually entered the information into Dell’s order fulfillment systems.

For Dell, the Internet was a sustaining technology. It made Dell’s core business processes work better, and it helped Dell make more money in the way it was structured to make money. But the identical strategy of selling directly to customers over the Internet was very disruptive relative to Compaq’s business model, because that company’s cost structure and business processes were targeted at in-store retail distribution.

The theory of disruption would conclude that if Dell (and Gateway) had not existed, then start-up Internet-based computer retailers might have succeeded in disrupting competitors such as Compaq. But because the Internet was sustaining to powerful incumbents, entrant Internet computer retailers have not prospered.

17.2.4 A Disruptive Business Model Is a Valuable Corporate Asset

A disruptive business model that can generate attractive profits at the discount prices required to win business at the low end is an extraordinarily valuable growth asset. When its executives carry the business model up-market to make higher-performance products that sell at higher price points, much of the increment in pricing falls to the bottom line-and it continues to fall there as long as the disruptor can keep moving up, competing at the margin against the higher-cost disruptee. When a company tries to take a higher-cost business model down-market to sell products at lower price points, almost none of the incremental revenue will fall to its bottom line. It gets absorbed into overheads. This is why established firms that hope to capture the growth created by disruption need to do so from within an autonomous business with a cost structure that offers as much headroom as possible for subsequent profitable migration up-market.

Moving up the trajectory into successively higher-margin tiers of the market and shedding less-profitable products at the low end is something that all good managers must do in order to keep their margins strong and their stock price healthy. Standing still is not an option, because firms that stop moving up find themselves in a rebar-esque situation, slugging it out with hard-to-differentiate products against competitors whose costs are comparable (footnote 12).

This ultimately means that in doing what they must do, every company prepares the way for its own disruption. This is the innovator’s dilemma. But it also is the beginning of the innovator’s solution. It does not guarantee success, but it sure helps: The Innovator’s Dilemma (Christensen 1997) showed that following a strategy of disruption increased the odds of creating a successful growth business from 6 to 37 percent (footnote 13). Because the established company’s course of action is mandated so clearly, it is also clear what executives who seek to create new-growth businesses should do: Target products and markets that the established companies are motivated to ignore or run away from. Many of the most profitable growth trajectories in history have been initiated by disruptive innovations.

17.3 Two Types of Disruption

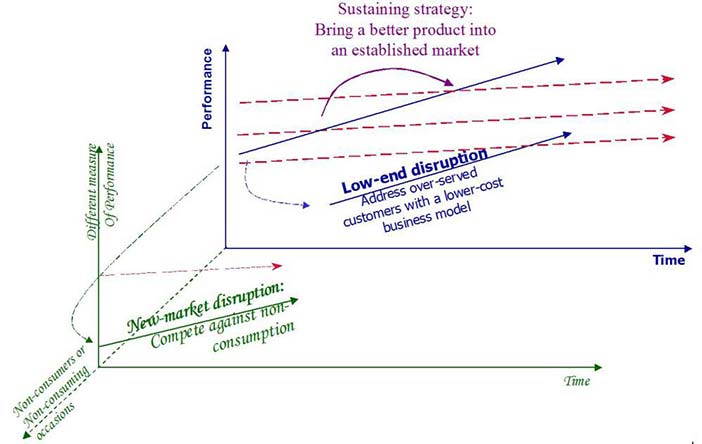

For the sake of simplicity, The Innovator’s Dilemma (Christensen 1997) presented the disruptive innovation diagram in only two dimensions. In reality, there are two different types of disruptions, which can best be visualized by adding a third axis to the disruption diagram, as shown in Figure 3. The vertical and horizontal axes are as before: the performance of the product on the vertical axis, with time plotted on the horizontal dimension. The third axis represents new customers and new contexts for consumption.

Our original dimensions-time and performance-define a particular market application in which customers purchase and use a product or service. In geometric terms, this application and set of customers reside in a plane of competition and consumption, which The Innovator’s Dilemma called a value network. A value network is the context within which a firm establishes a cost structure and operating processes and works with suppliers and channel partners in order to respond profitably to the common needs of a class of customers. Within a value network, each firm’s competitive strategy, and particularly its cost structure and its choices of markets and customers to serve, determines its perceptions of the economic value of an innovation. These perceptions, in turn, shape the rewards and threats that firms expect to experience through disruptive versus sustaining innovations (footnote 14).

The third dimension that extends toward us in the diagram represents new contexts of consumption and competition, which are new value networks. These constitute either new customers who previously lacked the money or skills to buy and use the product, or different situations in which a product can be used-enabled by improvements in simplicity, portability, and product cost. For each of these new value networks, a vertical axis can be drawn representing a product’s performance as it is defined in that context (which is a different measure from what is valued in the original value network).

Author/Copyright holder: Clayton Christensen. Copyright terms and licence: All Rights Reserved. Reproduced with permission. See section "Exceptions" in the copyright terms below.

Figure 17.3: Two Types of Disruptive Innovations

Different value networks can emerge at differing distances from the original one along the third dimension of the disruption diagram. In the following discussion, we will refer to disruptions that create a new value network on the third axis as new-market disruptions. In contrast, low-end disruptions are those that attack the least-profitable and most overserved customers at the low end of the original value network.

17.3.1 New-Market Disruptions

We say that new-market disruptions compete with “nonconsumption” because new-market disruptive products are so much more affordable to own and simpler to use that they enable a whole new population of people to begin owning and using the product, and to do so in a more convenient setting. The personal computer and Sony’s first battery-powered transistor pocket radio were new-market disruptions, in that their initial customers were new consumers-they had not owned or used the prior generation of products and services. Canon’s desktop photocopiers were also a new-market disruption, in that they enabled people to begin conveniently making their own photocopies right in their offices, rather than taking their originals to the corporate high-speed photocopy center where a technician had to run the job for them. When Canon made photocopying so convenient, people ended up making a lot more copies. New-market disruptors’ challenge is to create a new value network, where it is non-consumption, not the incumbent, that must be overcome.

Although new-market disruptions initially compete against non-consumption in their unique value network, as their performance improves they ultimately become good enough to pull customers out of the original value network into the new one, starting with the least-demanding tier. The disruptive innovation doesn’t invade the mainstream market; rather, it pulls customers out of the mainstream market into the new one because these customers find it more convenient to use the new product.

Because new-market disruptions compete against non-consumption, the incumbent leaders feel no pain and little threat until the disruption is in its final stages. In fact, when the disruptors begin pulling customers out of the low end of the original value network, it actually feels good to the leading firms, because as they move up-market in their own world, for a time they are replacing the low-margin revenues that they lose to the disruptors with higher-margin revenues (footnote 15).

17.3.2 Low-End Disruptions

We call disruptions that take root at the low end of the original or mainstream value network low-end disruptions. Disruptions such as steel minimills, discount retailing, and the Korean automakers’ entry into the North American market have been pure low-end disruptions in that they did not create new markets-they were simply low-cost business models that grew by picking off the least attractive of the established firms’ customers. Although they are different, new-market and low-end disruptions both create the same vexing dilemma for incumbents. New-market disruptions induce incumbents to ignore the attackers, and low-end disruptions motivate the incumbents to flee the attack.

Low-end disruption has occurred several times in retailing (footnote 16). For example, full-service department stores had a business model that enabled them to turn inventories three times per year. They needed to earn 40 percent gross margins to make money within their cost structure. They therefore earned 40 percent three times each year, for a 120 percent annual return on capital invested in inventory (ROCII). In the 1960s, discount retailers such as Wal-Mart and Kmart attacked the low end of the department stores’ market-nationally branded hard goods such as paint, hardware, kitchen utensils, toys, and sporting goods-that were so familiar in use that they could sell themselves. Customers in this tier of the market were overserved by department stores, in that they did not need well-trained floor salespeople to help them get what they needed. The discounters’ business model enabled them to make money at gross margins of about 23 percent, on average. Their stocking policies and operating processes enabled them to turn inventories more than five times annually, so that they also earned about 120 percent annual ROCII. The discounters did not accept lower levels of profitability-their business model simply earned acceptable profit through a different formula (footnote 17).

It is very hard for established firms not to flee from a low-end disruptor. Consider, for example, the choice that executives of full-service department stores had to make when the discount retailers were attacking the branded hard goods at the low end of department stores’ merchandise mix. Retailers’ critical resource allocation decision is the use of floor or shelf space. One option for department store executives was to allocate more space to even higher-margin cosmetics and high-fashion apparel, where gross margins often exceeded 50 percent. Because their business model turned inventories three times annually, this option promised 150 percent ROCII.

The alternative was to defend the branded hard goods businesses, which the discounters were attacking with prices 20 percent below those of department stores. Competing against the discounters at those levels would send margins plummeting to 20 percent, which, given the three-times inventory turns that were on average inherent in their business model, entailed a ROCII of 60 percent. It thus made perfect sense for the full-service department stores to flee-to get out of the very tiers of the market that the discounters were motivated to enter (footnote 18).

Many disruptions are hybrids, combining new-market and low-end approaches, as depicted by the continuum of the third axis in Figure 3. Southwest Airlines is actually a hybrid disruptor, for example. It initially targeted customers who weren’t flying-people who previously had used cars and buses. But Southwest pulled customers out of the low end of the major airlines’ value network as well. Charles Schwab is a hybrid disruptor. It stole some customers from full-service brokers with its discounted trading fees, but it also created new markets by enabling people who historically were not equity investors-such as students-to begin owning and trading stocks (footnote 19).

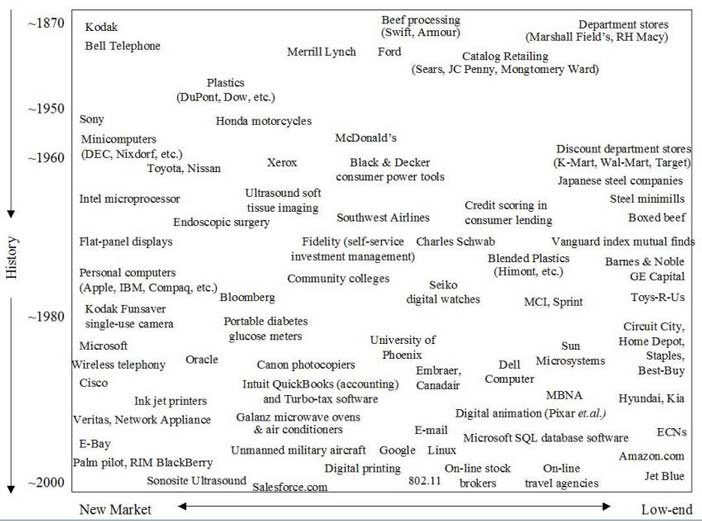

Figure 4 shows where some of history’s more successful disruptors were positioned along the continuum of new-market to low-end disruption at their inception. The appendix to this chapter offers a brief historical explanation of each of the disruptive products or companies listed on the chart. This is not a complete census of disruptive companies, of course, and their position on the chart is only approximate. However, the array does convey our sense that disruption is a primary wellspring of growth. The prevalence of Japanese companies such as Sony, Nippon Steel, Toyota, Honda, and Canon in the period between 1960 and 1980and the absence of new disruptive companies in the 1990s, for example, explain a lot about why Japan’s economy has stagnated. Many of its most influential companies grew dramatically by disrupting others; but the structure of Japan’s economic system inhibits the creation of new waves of disruptive growth that might threaten these same companies today (footnote 20).

The chart also shows that disruption is an ongoing force that is always at work-meaning that disruptors in one generation become disruptees later. The Ford Model T, for example, created the first massive wave of disruptive growth in automobiles. Toyota, Nissan, and Honda then created the next wave, and Korean automakers Hyundai and Kia have now begun the third. AT&T’s wireline long distance business, which disrupted Western Union, is being disrupted by wireless long distance. Plastics makers such as Dow, DuPont, and General Electric continue to disrupt steel, even as their low end is being eaten away by suppliers of blended polyolefin plastics such as Himont.

Author/Copyright holder: Clayton Christensen. Copyright terms and licence: All Rights Reserved. Reproduced with permission. See section "Exceptions" in the copyright terms below.

Figure 17.4: A Sampling of Companies Whose Origins Were in Disruption

17.4 Shaping Ideas to Become Disruptive: Three Litmus Tests

At the beginning of this chapter, we mentioned that few technologies or product ideas are inherently sustaining or disruptive when they emerge from the innovator’s mind. Instead, they go through a process of becoming fleshed out and shaped into a strategic plan in order to win funding. Many-but not all-of the initial ideas that get shaped into sustaining innovations could just as readily be shaped into disruptive business plans with far greater growth potential. The shaping process must be consciously managed, however, and not left in an autopilot mode.

Executives must answer three sets of questions to determine whether an idea has disruptive potential. The first explores whether the idea can become a new-market disruption. For this to happen, at least one and generally both of two conditions must be satisfied:

Is there a large population of people who historically have not had the money, equipment, or skill to do this thing for themselves, and as a result have gone without it altogether or have needed to pay someone with more expertise to do it for them?

To use the product or service, do customers need to go to an inconvenient, centralized location?

If the technology can be developed so that a large population of less skilled or less affluent people can begin owning and using, in a more convenient context, something that historically was available only to more skilled or more affluent people in a centralized, inconvenient location, then there is potential for shaping the idea into a new-market disruption.

The second set of questions explores the potential for a low-end disruption. This is possible if these two conditions exist:

Are there customers at the low end of the market who would be happy to purchase a product with less (but good enough) performance if they could get it at a lower price?

Can we create a business model that enables us to earn attractive profits at the discount prices required to win the business of these overserved customers at the low end?

Often, the innovations that enable low-end disruption are improvements in manufacturing, service, or business processes, which enable a company to earn attractive returns on lower gross margins, coupled with processes that turn assets faster.

Once an innovation passes the new-market or low-end test, there is still a third critical consideration, or litmus test, to apply:

Is the innovation disruptive to all of the significant incumbent firms in the industry? If it appears to be sustaining to one or more significant players in the industry, then the odds will be stacked in that firm’s favor, and the entrant is unlikely to win.

If an idea fails the litmus tests, then it cannot be shaped into a disruption. It may have promise as a sustaining technology, but in that case we would expect that it could not constitute the basis of a new-growth business for an entrant company.

For summary, table 1 contrasts the characteristics of the three strategies that firms might pursue in creating new-growth businesses: sustaining innovations, new-market disruptions, and low-end disruptions. It compares the targeted product performance or features, the targeted customers or markets, and the business model implications that each route entails. We hope that managers can use this as a template so that they can categorize and see the implications of different plans that might be presented to them for approval.

Executives can use this categorization and the litmus tests to foresee the competitive consequences of alternative strategies as they shape an idea. To illustrate, we’ll examine three questions: whether Xerox could disrupt Hewlett-Packard’s ink-jet printing business, how to create growth in air conditioning, and whether online banking had (or has) the disruptive potential to create a new-growth business.

Dimension | Sustaining Innovations | Low-end disruptions | New Market Disruptions |

Targeted performance of the product or service | Results in performance improvement in attributes most valued by the industry’s mainstream customers. These improvements may be incremental or breakthrough in character. | Technology yields products that are good enough along the traditional metrics of performance at the low end of the mainstream market. | Results in lower performance in “traditional” attributes, but improved performance in new attributes - typically simplicity and convenience. |

Targeted customers or market application | The most attractive (i.e., profitable) customers in the mainstream markets who are willing to pay for improved performance. | Targets over-served customers in the low end of the mainstream market. | Targets non- consumption: customers who historically lacked the money or skill to buy and use the product. |

Impact on the required business model (processes and cost structure) | Improves or maintains profit margins by exploiting the existing processes and cost structure, and making better use of current competitive advantages. | Utilizes a new operating and / or financial approach - a different combination of lower gross profit margins and higher asset utilization that can earn attractive returns at the discount prices required to win business at the low end of the market. | Business model must make money at lower price per unit sold, and at unit production volumes that initially will be small emerging market. Gross margin dollars per unit sold will be significantly lower. |

Table 17.1: Distinguishing Characteristics of Sustaining vs. Low-End and New-Market Disruptions

17.4.1 Could Xerox Disrupt Hewlett-Packard?

We don’t actually know if Xerox has considered the possibility of creating a new business of the sort we will examine here, and we use the companies’ names only to make the example more vivid. We’ve based this scenario solely on information from public sources. Xerox reportedly has developed outstanding ink-jet printing technology. What can it do with it? It could attempt to leapfrog Hewlett-Packard by making the best ink-jet printer on the market. Even if it could make a better printer, however, Xerox would be fighting a battle of sustaining technology against a company with superior resources and more at stake. HP would win that fight. But could Xerox craft a disruptive strategy for this technology? We’ll test the conditions for a low-end strategy first.

To determine whether this strategy is viable, Xerox’s managers should test whether customers in the lowest market tiers might be willing to buy a “good enough” printer that is cheaper than prevailing products (footnote 21). At the highest tier of the market, customers seem willing to pay significantly more for a faster printer that produces sharper images. However, consumers in the less-demanding tiers are becoming increasingly indifferent to improvements. It is likely they would be interested in lower-cost alternatives. So the first question gets an affirmative answer.

The next question is whether Xerox could define a business model that could generate attractive returns at the discounted prices required to win business at the low end. The possibilities here don’t look good. HP and other printer companies already outsource the fabrication and assembly of components to the lowest-cost sources in the world. HP makes its money selling ink cartridges-whose fabrication also is outsourced to low-cost suppliers. Xerox could enter the market by selling ink cartridges at lower prices, but unless it could define an overhead cost structure and business processes that would allow it to turn assets faster, Xerox could not sustain a strategy of low-end disruption (footnote 22).

This means we’ll need to evaluate the potential for a new-market disruption-competing against non-consumption. Is there a large, untapped population of computer owners who don’t have the money or skill to buy and use a printer? Probably not. Hewlett-Packard already competed successfully against non-consumption when it launched its easy-to-use, inexpensive ink-jet printers

What about enticing existing printer owners to buy more printers, by enabling consumption in a new, more convenient context? Now, this might be achievable. Documents created on notebook computers are not easy to print. Notebook users have to find a stationary printer and connect to it either over a network or a printer cable, or they must transfer the file via removable media to a computer that is connected to a printer. If Xerox incorporated a lightweight, inexpensive printer into the base or spine of a notebook computer so that people on the go could get hard copies when and where they needed them, the company could probably win customers even if the printer wasn’t as good as a stationary ink-jet printer. Only Xerox’s engineers could determine whether the idea is technologically feasible. But as a strategy, this would pass the litmus tests.

If Xerox attempted this, we would expect HP to ignore this new-market disruption at the outset because the market would be much smaller than the stationary printer market. HP’s printer business is huge, and the company needs large sources of new revenue to sustain its growth. To trap Hewlett-Packard in an innovator’s dilemma, Xerox should develop a business model that’s attractive to Xerox but unattractive to the managers of HP and other leading established printer companies. This might entail pricing ink cartridges for embedded notebook printers low enough that the executives of HP’s ink jet printer business would find the market unattractive relative to investments they might make to move up-market in search of the higher profits they could find by competing against higher-cost stationary laser printers.

17.4.2 Conditions for Growth in Air Conditioners

The window-mounted air conditioner market is widely known to be mature, dominated by giants such as Carrier and Whirlpool. Could a company like General Electric (GE) wallop them? We would predict GE’s defeat if it tried to enter this market with a quieter product that offered more features and better energy efficiency (footnote 23). Is a low-end disruption viable? Our sense is that there are overserved customers at the low end of the existing market. They signal their overservedness by opting for the least-expensive models they can find, unwilling to pay premium prices for the alternative products that are available to them. GE might expand its already substantial manufacturing operations in China, making air conditioners for export to developed economies. This might bring modest but temporary success, because after the established companies respond by setting up their own manufacturing operations in China, GE would find itself locked in a battle with competitors whose costs are comparable and whose distribution and service infrastructure are strong, and where the targeted customers already have manifested an unwillingness to pay premium prices for better products. Employing low-cost labor constitutes a low-cost business model only until competitors avail themselves of the same option.

How about a new-market disruption, however? There are hundreds of millions of non-consumers of residential air conditioning in China, who have been blocked from that market because the power-hungry, expensive machines that historically have been available don’t fit in the average family’s pocketbook or apartment. If GE could design a $49.95 product that would easily slip into the window of a cramped Shanghai apartment and reduce the temperature and humidity in a ten-foot by ten-foot room with ten amps of current, things might get interesting-because once GE had a business model that could make money at that price point, taking on the rest of the up-market world would be easy. Parenthetically, while Western executives are understandably concerned about the threat that low-cost manufacturing in China poses to them, our guess is that China’s greatest competitive asset is the unfathomable amount of non-consumption in its markets, which makes them fertile ground for new-market disruptive companies of many sorts.

17.5 Afterword

Disruption is a theory: a conceptual model of cause and effect that makes it possible to better predict the outcomes of competitive battles in different circumstances. The asymmetries of motivation chronicled in this chapter are natural economic forces that act on all businesspeople, all the time. Historically, these forces almost always have toppled the industry leaders when an attacker has harnessed them, because disruptive strategies are predicated upon competitors doing what is in their best and most urgent interest: satisfying their most important customers and investing where profits are most attractive. In a profit-seeking world, this is a pretty good bet.

Not all innovative ideas can be shaped into disruptive strategies, however, because the necessary preconditions do not exist; in such situations, the opportunity is best licensed or left to the firms that are already established in the market. On occasion, entrant companies have simply caught the leaders asleep at the switch and have succeeded with a strategy of sustaining innovation. But this is rare. Disruption does not guarantee success: It just helps with an important element in the total formula.

17.6 Acknowledgements

This chapter is adapted from the author’s book, The Innovator's Solution, isbn 1578518520

[Editor's note: We highly recommend this seminal book. Published in 2003, it is still as relevant today as in 1997, and has had tremendous impact on how we think about - and practice - innovation worldwide.]

17.7 Appendix: A Brief Description of the Disruptive Strategies of the Firms in Figure 4

Table 2 briefly summarizes our understanding of the disruptive roots of the success of the companies that are arrayed in Figure 4. Because of space limitations, much important detail has been omitted. The companies are listed in alphabetical, rather than chronological, order. We do not pretend to be strong business historians, and as a consequence can only present here a partial listing of disruptive companies. Furthermore, it is often difficult to identify a specific year in which each firm’s disruptive strategy was launched. Some firms existed for a considerable period, often in other lines of business, before the disruptive strategy that led to their ultimate success was implemented. In some cases it seems easier to visualize the disruption in terms of a product category, rather than by listing the name of one company. Hence, we ask our readers to regard this information as only suggestive, rather than definitive.

Company or Product | Description |

802.11 | This is a protocol for high bandwidth wireless transfer of data. It has begun disrupting local area wireline networks. Its present limitations are that the signals can’t travel long distances. |

Amazon.com | A low-end disruption relative to traditional bookstores. |

Apple, Compaq et.al., Personal computers | Microprocessor-based computers made by firms such as Apple, IBM and Compaq were true new-market disruptions, in that for years they were sold and used in their unique value network before they began to capture sales from higher-end professional computers. |

Beef Processing | In the 1880s, Swift and Armour began huge, centralized beef slaughtering operations that transported large sides of beef by refrigerated railcar to local meat cutters. This disrupted local slaughtering operations. |

Bell Telephone | Bell’s original telephone could only carry a signal for 3 miles, and therefore was rejected by Western Union, whose business was long-distance telegraphy, because Western Union couldn’t use it. Bell therefore started a new-market disruption, offering local communication - and as the technology improved, it pulled customers out of telegraphy’s long distance value network into telephony. |

Black & Decker | Prior to 1960, hand-held electric tools were heavy and rugged, designed for professionals - and very expensive. B&D introduced a line of plastic-encased tools with universal motors that would only last 25-30 hours of operation - which actually was more than adequate for most do-it-yourselfers who drill a few holes per month. In today’s dollars, B&D brought the cost of these tools down from $150 to $20, enabling a whole new population to own and use their own tools. |

Blended Plastics | These blends of inexpensive polyolefin plastics like polypropylene, sold by firms like Himont, create composite materials that in many ways share the best properties of their constituent materials. They are getting better at a stunning rate, disrupting markets that historically had been the province of engineering polycarbonate plastics made by firms like GE Plastics. |

Bloomberg LP | Bloomberg began by providing basic financial data to investment analysts and brokers. It gradually has improved its data offerings and analysis, and subsequently moved into the financial news business. It has substantially disrupted Dow Jones and Reuters as a result. More recently it has created its own ECN to disrupt stock exchanges. Issuers of government securities can auction their initial offerings over the Bloomberg system, disrupting investment banks. |

Boxed beef | The “boxed beef” model of Iowa Beef Packers completed the disruption of local butchering operations. Instead of shipping large sides of beef to local meat cutters for further cutting, IBP cut the beef into finished or nearly finished cuts, for placement directly in supermarket cases. |

Canon photocopiers | Until the early 1980s when we needed photocopiers, we had to take our originals to the corporate photocopy center, where a technician ran the job for us. He had to be a technician, because the high-speed Xerox machine in there was very complicated, and needed servicing frequently. When Canon and Ricoh introduced their countertop photocopiers, they were slow, produced poor-resolution copies, and didn’t enlarge or reduce or collate. But they were so inexpensive and simple to use that we could afford to put one right around the corner from our office. At the beginning we still took our high-volume jobs to the copy center. But little by little Canon improved its machines to the point that today, immediate, convenient access to high-quality, full-featured copying is almost a constitutional right in most workplaces. |

Catalog retailing | Sears, Roebuck and Montgomery Ward took root as catalog retailers - enabling people in rural America to buy things that historically had not been accessible. Their business model, entailing annual inventory turns of 4x and gross margins of 30%, was disruptive relative to the model of full-service department stores, which relied upon 40% gross margins because they turned inventories only 3x annually. Sears and Wards later moved up-market, building retail stores. |

Charles Schwab | Started in 1975 as one of the first discount brokers. In the late 1990s Schwab created a separate organization to build an on-line trading business. It was so successful that the company shut down its original organization of telephone brokers. |

Circuit City, Best Buy | Disrupted the consumer electronics departments of full-service and discount department stores, which has sent them up-market into higher-margin clothing. |

Cisco | Cisco’s router uses packet-switching technology to direct the flow of information over the telecommunications system, compared to the circuit-switching technology of the established industry leaders such as Lucent, Siemens and Nortel. The technology divides information into virtual “envelopes” called packets, and sends them out over the Internet. Each packet might take a different route to the addressed destination; and when they arrive, the packets are put in the right order and “opened” for the recipient to see. Because this process entailed a few seconds’ latency delay, packet switching could not be used for voice telecommunications. But it was good enough to enable a new market to emerge - data networks. The technology has improved to the point that today, the latency delay of a packet-switched voice call is almost imperceptibly slower than that of a circuit-switched call - enabling VOIP, or voice-over-Internet-protocol telephony. |

Community colleges | In some states, up to 80% of the graduates of reputable four-year state universities took some or all of their required general education courses at much less expensive community colleges, and then transferred those credits to the university - which (unconsciously) is becoming a provider of upper-division courses. Some community colleges have begun offering four-year degrees. Their enrollment is booming, often with non-traditional students who otherwise would not have taken these courses. |

Concord School of Law | Founded by Kaplan, a unit of the Washington Post Company, this on-line law school has attracted a host of (primarily) non-traditional students. The school’s accreditation allows its graduates to take the California Bar exam, and its graduates’ success rate is comparable to those of many other law schools. Many of its students don’t enroll to become lawyers, however. They want to understand law to help them succeed in other careers. |

Credit scoring | A formulaic method of determining creditworthiness, substituting for the subjective judgments of bank loan officers. Developed by a Minneapolis firm, Fair Isaac. Used initially to extend Sears and Penny’s in-store credit cards. As the technology improved, it was used for general credit cards, and then auto, mortgage and now small business loans. |

Dell Computer | Dell’s direct-to customer retailing model and its fast-throughput, high asset-turns manufacturing model allowed it to come underneath Compaq, IBM and Hewlett Packard as a low-end disruptor in personal computers. Clayton Christensen, the quintessential low-end consumer, wrote his doctoral thesis on a Dell notebook computer purchased in 1989, because it was the cheapest portable computer on the market. Because of Dell’s reputation for marginal quality, students needed special permission from Harvard to use doctoral stipend money to buy a Dell rather than a computer with a more reputable brand. Today Dell supplies most of the Harvard Business School’s computers. |

Department Stores | Department stores like Z.C.M.I. in Salt Lake City, Marshall Field in Chicago, and R.H. Macy in New York, disrupted small shopkeepers. The department stores made money by accelerating inventory turns to 3x per year, which enabled them to earn attractive profit with 40% gross margins. Because their salespeople were much less knowledgeable about products, at the outset department stores had to start at the simplest end of the merchandise mix, with products that were so familiar in use that they “sold themselves.” |

Digital animation | The fixed cost and skill required to make a full-length animated movie historically was so high that almost nobody could do it except Disney. Digital animation technology now enables far more companies (Such as Pixar) to compete against Disney. |

Discount department stores | Department stores like Korvette’s in New York, K-Mart in Detroit, and later Wal-Mart and Target disrupted full-service department stores. The discount stores made money by accelerating inventory turns to 5x per year, which enabled them to earn attractive profit with 23% gross margins. Because their salespeople were much less knowledgeable about products, at the outset the discount department stores had to start at the simplest end of the merchandise mix, with branded hard goods that were so familiar in use that they “sold themselves.” They subsequently have moved up-market into soft goods such as clothing. |

E-Bay | Most of the Internet start-ups of the late 1990s attempted to use the Internet as a sustaining innovation relative to the business models of established companies. E-Bay was a notable exception, as it pursued a new-market disruptive strategy - enabling owners of collectibles that could never turn the head of auction house executives, now to be able to sell off things that they no longer needed. |

ECNs | Electronic clearing networks (ECNs) allow buyers and sellers of equities to exchange them over a computer, at a fraction of the cost of doing it on a formal stock exchange. Island, one of the leading ECNs, can handle on one workstation volume amounting to 20% of the NASDAQ’s volume. |

E-mail is disrupting postal services around the globe. The volume of personal communication that is done by letter is dropping precipitously, leaving postal services with magazines, bills and junk mail. | |

Embraer & Canadair regional jets | The regional passenger jet business is booming, as their capacity over the past 15 years has stretched from 30 to 50, 70 and now 106. As Boeing and Airbus struggle to make bigger, faster jets for transcontinental and transoceanic travel, their growth has stagnated; the industry has consolidated (Lockheed and McDonnell Douglas have been folded in); and the growth is at the bottom of the market. |

Endoscopic Surgery | Minimally invasive surgery was actively disregarded by leading surgeons because the technique could only address the simplest procedures. But it has improved to the point that even certain relatively complicated heart procedures are done through a small port. The disruptive impact has primarily been on equipment makers and hospitals. |

Fidelity management | Created “self-service” personal financial management through its easy-to-buy families of mutual funds, 401k accounts, insurance products, etc. Fidelity was founded a few years after WWII; but began its disruptive movements in the 1970s, as best we can tell. |

Flat panel displays (Sharp et.al.) | We normally think of disruptive technologies as being inexpensive, and many people are puzzled at how we could call flat panel displays disruptive. Haven’t they come from the high end? Actually, no. Flat panel LCD displays took root in digital watches; and then moved to calculators, notebook computers and small portable televisions. These were applications that historically had no electronic displays at all, and LCD displays were much cheaper than alternative means of bringing imaging to those applications. Flat screens have now begun invading the mainstream market of computer monitors and in-home television screens, disrupting the cathode ray tube. They are able to sustain substantial premium prices because of their 2-D character. |

Ford | Henry Ford’s Model T was so inexpensive that he enabled a much larger population of people who historically could not afford cars, now to own one. |

Galanz | China’s Galanz captured nearly 40% of the world microwave oven market in the 1990s. While the company could have followed a strategy of low-end disruption - using low-cost Chinese labor to make appliances for export, it instead chose to be a new-market disruptor, making ovens that were small enough and consumed little-enough power to be used in cramped Chinese apartments; and were cheap enough for non-microwave oven owners to afford. Once they had built a business model that could make market-enabling price points for the domestic Chinese market, then taking on the rest of the world was as easy as egg-drop soup. |

GE Capital | Has disrupted major portions of the commercial banks’ historical markets, primarily through low-end disruptive strategies. |

Google and its competing Internet search engines are disrupting directories of many sorts, including the Yellow Pages. | |

Honda motorcycles | Honda’s Supercub, introduced in the late 1950s, disrupted makers of big, thunderous motorcycles such as Harley Davidson, Triumph, BMW and many others. It took root as an off-road recreational motorized bicycle, and then improved. Honda was joined by Yamaha, Kawasaki and Suzuki. |

Ink jet printers | These were a disruption to the laser jet printer, and a sustaining technology relative to the dot-matrix printer. We put ink jet printers toward the “new market” end of the disruption spectrum, because their compact size, light weight and low initial cost enabled a whole population of computer owners - primarily students - each to own and use a printer. While they were slow and produced fuzzy images at the outset, ink jet printers are now the mainstream printer of choice, having pushed laser jets to the high end. Hewlett Packard stayed atop this industry by setting up an autonomous ink jet business unit to compete against its laser jet printer business. |

Intel micro-processor | Intel’s earliest microprocessor in 1971 could only constitute the brain of a four-function calculator. Makers of computers whose logic circuitry is microprocessor-based have disrupted firms that made mainframe and minicomputers, whose logic circuitry was printed wiring board-based. |

Intuit’s QuickBooks accounting software | Whereas the established industry leaders in accounting software enabled small business managers to run all sorts of sophisticated reports for analytical purposes, QuickBooks, which was a derivative of Intuit’s personal finance software product Quicken, basically helped them keep track of their cash. It created a huge new market amongst very small business owners (most less than five employees) who historically did not keep their books on computer. Within two years of launch Intuit had seized 85% of the small business accounting software market - mainly by creating new growth. The stealing of the established companies’ customers came later, as QuickBooks’ functionality improved. |

Intuit’s Turbotax | PC-based accounting software is disrupting personal tax preparation services such as H&R Block. |

Japanese Steel Makers | Firms like Nippon Steel, Nippon Kokkan and Kobe and Kawasaki Steel began their growth by exporting very low quality steel to western markets starting in the late 1950s. As their customers (including disruptive Japanese auto makers like Toyota) grew, the Japanese steel industry had to increase capacity dramatically, enabling it to incorporate the latest steelmaking technology like continuous casting and basic oxygen furnaces in the new mills. This accelerated their up-market trajectory dramatically. |

Jet Blue | Whereas Southwest Airlines initially followed a strategy of new-market disruption, Jet Blue’s approach is low-end disruption. Its long-range viability depends upon the major airlines’ motivation to run away from the attack, as integrated steel mills and full-service department stores did. |

Kodak | Until the late 1800s, photography was extremely complicated. Only professionals could own and operate the expensive equipment. George Eastman’s simple “point and shoot” “Brownie” camera allowed consumers to take their own pictures. They could then mail the encased roll of film to Kodak, which would develop and return the photos by mail. |

Kodak Funsaver | Kodak’s Funsaver-brand single-use camera was born out after painful labor within Kodak, because its profit model - gross margins - were lower than Kodak could earn by selling roll film; and the quality of the images was not as good as those taken in high-quality 35mm cameras. But Kodak commercialized it through a different division, and it sold almost exclusively to people who would not have bought film anyway - because they didn’t have a camera. While it has potential to move up-market taking share against traditional cameras with a new brand, Maxx, we sense that Kodak has stopped driving it in this direction. |

Korean auto manufacturers: Hyundai & Kia | Korean automakers, including Hyundai and Kia, gained more points of worldwide market share in the 1990s than any other country’s automakers. And yet few of the established firms are concerned, because their gains have come in what is, to them, the lowest-profit portion of the market. |

MBNA | We noted above that credit scoring is a formulaic method of determining the creditworthiness of a loan applicant. It was originally implemented in commercial banks as a sustaining technology - to reduce their costs of credit evaluation. In the 1990s, however, it was deployed in high-volume, low-cost “monoline” business models by firms such as MBNA, Capital One and First USA, which have substantially disrupted commercial banks’ credit card business. At the time of this writing, in fact, Citibank is the only major commercial bank with a substantial and profitable credit card business. |

McDonald’s | The fast food industry has been a hybrid disruptor, making it so inexpensive and convenient to eat out that they created a massive wave of growth in the “eating out” industry. Their earliest victims were “mom-and-pop” diners. In the last decade the advent of food courts has taken fast food up-market. Expensive, romantic high-end restaurants still thrive at the high end, of course. |

MCI, Sprint | These firms were low-end disruptors relative to AT&T’s long distance telephone business. They enjoyed a unique opportunity to do this, because AT&T’s long distance rates were set by regulation at artificially high levels, in order to subsidize local residential telephone service. |

Merrill Lynch | Charles Merrill’s mantra in 1912 was to “Bring Wall Street to Main Street.” By employing salaried rather than commissioned brokers, he made it inexpensive enough to trade stocks that middle-income Americans could become equity investors. Merrill Lynch moved up-market over the next 90 years towards higher net worth investors. Most of the brokerage firms that held seats on the New York Stock exchange in the 1950s and 60s have been merged out of existence, because Merrill Lynch disrupted them. |

Microsoft | Its operating system was inadequate versus those of mainframe and minicomputer makers; versus Unix; and versus Apple’s system. But its migration from DOS to Windows to Windows NT is taking the firm up-market, to the point that the Unix world is seriously threatened. Microsoft, in turn, faces a threat from Linux. |

Mini-computers | Companies like Digital Equipment, Prime, Wang, Data General and Nixdorf were new-market disruptors relative to mainframe computer makers. Their relative simplicity and low price enabled departments (particularly engineering) in organizations to have their own computers, instead of having to rely on inconvenient, centralized mainframe computers that typically were optimized for generating financial reports. |

On-line stock brokers | On-line trading of equities is a sustaining technology relative to the business models of discount brokers such as Ameritrade, and is disruptive relative to full-service brokers such as Merrill Lynch. For Schwab, which started as a bare-bones discount broker but had moved up towards the mainstream market by the mid-1990s, Internet-based trading was disruptive enough that the company had to set up a separate division. |

On-line travel agencies | Enabled by electronic ticketing, on-line travel agencies such as Expedia and Travelocity have so badly disrupted full-service, bricks-and-mortar agencies such as American Express that many airlines have dramatically cut the substantial commissions that historically they had paid to travel agencies. |

Oracle | Oracle’s relational database software was disruptive relative to that of the prior leaders, Cullinet and IBM, whose hierarchical or transactional database software ran on mainframe computers and was used to generate standard financial reports. Relational databases ran on minicomputers (and then microprocessor-based computers). Users without deep programming expertise could readily create their own custom reports and analyses using Oracle’s modular, relational architecture. |

Palm Pilot, RIM BlackBerry | Hand-held devices are new-market disruptions relative to notebook computers. |

Plastics | Plastics as a category have disrupted steel and wood, in that the “quality” of plastic parts often was inferior to those of wood and steel, along the metrics by which performance was measured in traditional applications. But their low cost and ease of shaping created many new applications, and plastics have pulled many applications out of the original metal and wood value networks into the plastic network. The disruption is particularly obvious if you look at where plastics were used in automobiles 30 years ago, versus today. |

Portable diabetes blood glucose meters | Disrupted makers of large blood glucose testing machines in hospital laboratories, enabling patients with diabetes to monitor their own glucose levels. |

Salesforce.com | This company, with its inexpensive, simple Internet-based system, is disrupting the leading providers of customer relationship management software like Siebel Systems. |

Seiko watches | Remember when Seiko watches were those cheap, throw-away black plastic watches? They, Citizen and Texas Instruments (which subsequently exited) disrupted the American and European watch industries. |

Sonosite | This firm makes a hand-held ultrasound device that enables healthcare professionals who historically needed the assistance of highly trained technicians with expensive equipment, now to look inside the bodies of patients in their care, and thereby to provide more accurate and timely diagnoses. The company floundered for a time attempting to implement its product as a sustaining innovation. But as of the time this book was being written, it seemed to have caught its disruptive stride in an impressive way. |

Sony | Sony pioneered the use of transistors in consumer electronics. Its portable radios and portable televisions disrupted firms like RCA that made large TVs and radios using vacuum tube technology. During the 1960s and 1970s, Sony launched a series of new-market disruptions, with products like video tape players, hand-held consumer video recorders, cassette tape players, the Walkman, and the 3.5-inch floppy disk drive. |

Southwest Airlines | It was a hybrid disruptor because its original strategy was to compete against driving and busses, and to fly in and out of non-mainstream airports. In addition, because its prices were so low it also took business from established airlines. Just as Wal-Mart enjoys profit protection from being in small towns whose market can only support one discount store, many of Southwest’s routes offer the same protection. |

SQL database software | Microsoft’s SQL database software product is disrupting Oracle, which has moved up-market into expensive, integrated enterprise systems. |

Staples | With its direct competitors Office Max and Office Depot, Staples disrupted small stationery stores as well as business-to-business office supplies distributors. |

Steel minimills | Have been disrupting integrated mills around the world since the mid-1960s, as recounted in the text. |

Sun Microsystems | Sun, Apollo (HP) and Silicon Graphics, which built their systems around RISC microprocessors, took root in essentially the same value network as minicomputers, and disrupted them. These firms, in turn, are now being disrupted by CISC microprocessor-based computer makers such as Compaq and Dell. |

Toyota | Entered the US market with cheap sub-compact cars like the Corona. These were so inexpensive that people who historically couldn’t afford a new car now could buy one; or families could acquire a second car. Toyota now makes Lexuses, you may have noticed. Nissan has migrated from its Datsun to Infiniti; and Honda has progressed from its miniature CVCC to Accura. |

Toys-R-Us | Disrupted the toy departments of full-service and discount department stores, which has sent them up-market into higher-margin clothing. |

Ultrasound | Ultrasound technology is disruptive, relative to X-Ray imaging. Hewlett Packard, Accuson, and ATL created a multi-billion-dollar industry by imaging soft tissues, which traditional X-ray technology could not capture. The leading X-Ray equipment makers, including General Electric, Siemens and Philips, became leaders in the two major radical sustaining technology revolutions in imaging: CT scanning and magnetic resonance imaging (MRI). Because ultrasound was a new market disruption, none of the X-ray companies participated in ultrasound until very recently, when they acquired major ultrasound equipment companies. |

University of Phoenix | A unit of Apollo, the University of Phoenix is disrupting four-year colleges and certain professional graduate programs. It began by providing employee training courses for businesses, often de facto, but sometimes by formal contract. Its programs have expanded into a variety of open-enrollment, degree-granting programs. Today it is one of the largest educational institutions in the United States, and is one of the leading providers of on-line education. |

Unmanned aircraft | These machines took root initially as drone targets to uncover hidden anti-aircraft emplacements. They then moved up-market into surveillance roles, and in the 2001-02 war in Afghanistan, moved for the first time into limited weapons-carrying roles. |

Vanguard | Index mutual funds have been a low-end disruption relative to managed mutual funds. At the time of this writing, Vanguard’s assets had grown to rival closely those of the former undisputed mutual fund leader, Fidelity management. |